🏡 Comparing Mortgage Types: Which Home Loan Is Right for You?

Choosing the right mortgage is one of the most important financial decisions homebuyers will make. With several loan types available—each offering different benefits, requirements, and long-term costs—it’s essential to understand the differences before locking in your financing. Whether you’re buying your first home or upgrading to your forever property, comparing mortgage types can help you save money and secure the best possible terms.

🔍 Why Choosing the Right Mortgage Matters

Your mortgage affects:

- Your monthly payment

- How much interest you pay over time

- The amount required for a down payment

- Your ability to refinance later

- The flexibility of your loan terms

Because every buyer’s financial situation is unique, the ideal mortgage varies from person to person. Below is a breakdown of the most common mortgage types and how they compare.

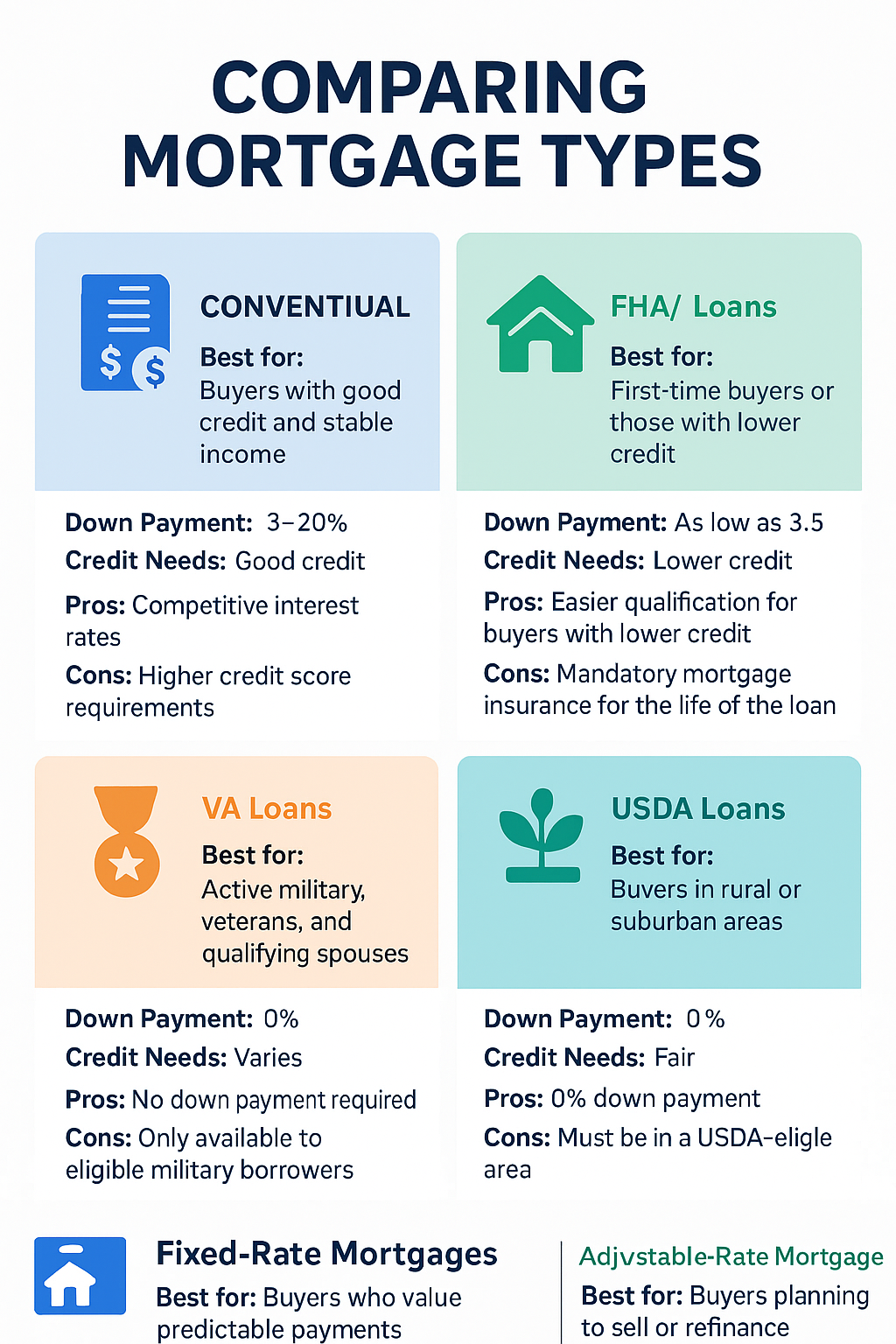

📘 1. Conventional Loans

Best for: Buyers with good credit and stable income

Conventional mortgages are not backed by the government. They usually offer:

- Competitive interest rates

- Lower overall borrowing costs

- Flexibility in loan terms

Pros:

- Good for strong credit scores

- Smaller long-term cost if credit is excellent

- Can remove PMI after reaching 20% equity

Cons:

- Higher credit score requirements

- Larger down payment may be needed

🏛️ 2. FHA Loans

Best for: First-time buyers or those with lower credit

FHA loans are backed by the Federal Housing Administration and aim to make homeownership more accessible.

Pros:

- Lower down payments (as low as 3.5%)

- Easier qualification for buyers with lower credit

- More lenient debt-to-income ratios

Cons:

- Mandatory mortgage insurance for the life of the loan

- Lower loan limits in some areas

🎖️ 3. VA Loans

Best for: Active military, veterans, and qualifying spouses

Backed by the Department of Veterans Affairs, VA loans are one of the most valuable benefits for military service members.

Pros:

- No down payment required

- No private mortgage insurance (PMI)

- Competitive interest rates

Cons:

- Only available to eligible military borrowers

- Mandatory funding fee (can be financed)

🌱 4. USDA Loans

Best for: Buyers in rural or suburban areas

USDA loans are backed by the U.S. Department of Agriculture and are designed to support rural homeownership.

Pros:

- 0% down payment

- Low mortgage insurance costs

- Good interest rates

Cons:

- Must be located in USDA-eligible areas

- Household income limits apply

🔒 5. Fixed-Rate Mortgages

Best for: Buyers who value predictable payments

In a fixed-rate mortgage, your interest rate stays the same for the entire loan term.

Pros:

- Stable monthly payments

- Protection from rising interest rates

- Ideal for long-term homeowners

Cons:

- Slightly higher initial rate compared to adjustable loans

🔄 6. Adjustable-Rate Mortgages (ARMs)

Best for: Buyers planning to sell or refinance within a few years

ARMs typically begin with a low rate that adjusts periodically based on market conditions.

Pros:

- Lower initial interest rate

- Good option for short-term living plans

Cons:

- Rates can rise significantly

- Less predictability over time

🧮 Which Mortgage Type Should You Choose?

The best mortgage depends on your:

- Credit score

- Down payment capabilities

- Long-term financial goals

- Military service status

- Planned time in the home

- Income and debt levels

Here’s a quick comparison summary:

| Mortgage Type | Down Payment | Credit Needs | Best For |

|---|---|---|---|

| Conventional | 3–20% | Good credit | Most buyers with stable finances |

| FHA | 3.5% | Low–fair credit | First-time buyers |

| VA | 0% | Varies | Military borrowers |

| USDA | 0% | Fair | Rural & suburban areas |

| Fixed-Rate | Varies | Any | Long-term planning |

| ARM | Low initially | Good credit | Short-term buyers |

🏁 Final Thoughts

Comparing mortgage types is the key to choosing the financing option that best supports your long-term financial goals. A loan that works for one buyer may not be ideal for another. Before applying, review your budget, how long you plan to stay in the home, and what monthly payment you’re comfortable with. A qualified mortgage professional can guide you through the options and help you secure the best possible rate.