Foreclosure and Short Sale Tips: Navigating Difficult Real Estate Situations

Facing foreclosure or considering a short sale can be stressful and overwhelming. These situations often arise from financial hardships, but with the right knowledge and strategies, homeowners can minimize damage and find the best possible outcome. This guide provides essential tips to help you navigate foreclosure and short sale processes effectively.

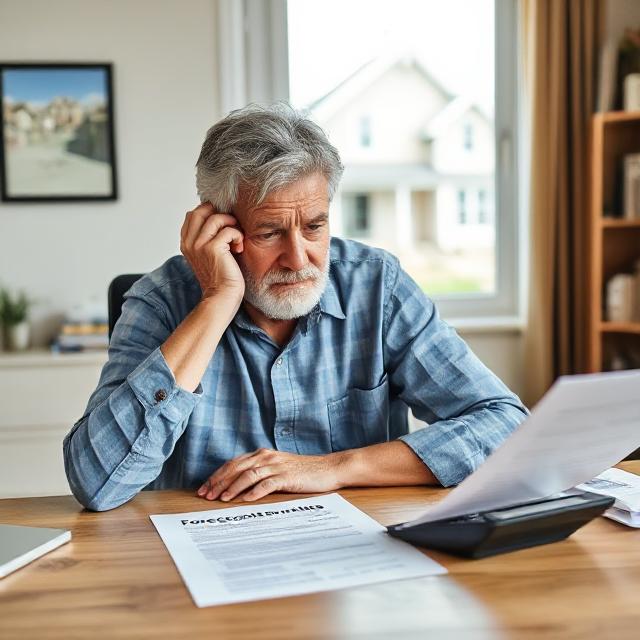

What Is Foreclosure?

Foreclosure occurs when a homeowner fails to make mortgage payments, prompting the lender to seize and sell the property to recover the owed debt. It typically involves a legal process that can take several months and significantly impact your credit score.

What Is a Short Sale?

A short sale happens when a homeowner sells their property for less than the remaining mortgage balance, with the lender’s approval. This option can help avoid foreclosure, but it requires lender approval and may take time to process.

Tips for Dealing with Foreclosure

1. Communicate Early with Your Lender

As soon as you anticipate payment difficulties, contact your lender. Many lenders offer hardship programs, loan modifications, or repayment plans.

2. Explore Loan Modification Options

Request a loan modification to reduce your interest rate, extend your loan term, or lower your monthly payments. This can make payments more manageable.

3. Seek Financial Counseling

Consult a HUD-approved housing counselor for guidance tailored to your situation. They can help you explore options and negotiate with lenders.

4. Consider a Deed-in-Lieu of Foreclosure

If you can’t keep up with payments, some lenders accept a deed-in-lieu, where you voluntarily transfer ownership to avoid foreclosure proceedings. This may impact your credit but can be less damaging than a foreclosure.

Tips for a Successful Short Sale

1. Act Quickly

If you’re behind on payments and the market value is less than your mortgage, consider a short sale before foreclosure proceedings begin.

2. Work with an Experienced Real Estate Agent

A knowledgeable agent can help you list the property, negotiate with the lender, and navigate the complex short sale process.

3. Gather Necessary Documentation

Lenders typically require proof of financial hardship, such as tax returns, bank statements, and hardship letters.

4. Be Honest and Transparent

Open communication with your lender and potential buyers increases the chances of a successful short sale.

5. Understand the Impacts

While a short sale can help avoid foreclosure, it still affects your credit score and may have tax implications. Consult a financial advisor before proceeding.

Final Thoughts

Facing foreclosure or considering a short sale is challenging, but proactive steps and professional guidance can help you minimize financial damage and explore options for recovery. Remember, the goal is to protect your credit and financial future while working through these difficult situations.

If you’re in this situation, act promptly, seek professional advice, and explore all available options. Your financial recovery is possible.